Should Britain Drill, Baby, Drill? The North Sea Question in Plain English

A 10-minute read on whether ramping up oil and gas extraction would actually fix anything

A 10-minute read on whether ramping up oil and gas extraction would actually fix anything

In short

A growing political argument holds that Britain should drop its renewables push, increase North Sea production, and reclaim its energy freedom. The pitch is straightforward in its appeal: our oil, our gas, our prices, our jobs.

The numbers do not really support it. The North Sea is roughly 93% drained. What remains is expensive to extract, mostly destined for export, and would do little to your gas bill, because oil and gas are sold at global prices set in places such as Rotterdam and Singapore. Even Norway, with twenty times more state-controlled production than the UK, paid European prices during the energy crisis.

Renewables are not a complete answer either. Wind does not blow on demand, and the grid still relies on gas to fill the gaps. The economics, though, have shifted considerably. New offshore wind now undercuts new gas-fired power, batteries are scaling quickly, and the UK already draws more than half its electricity from clean sources.

What follows is the case in plain English, with the evidence set out so you can weigh it for yourself.

What the political pitch actually says

The argument runs roughly as follows:

- Wind and solar are intermittent, so we will always need backup

- Britain still has substantial oil and gas under the North Sea

- Domestic production means energy independence and protection from world prices

- Net zero is making us poorer, so we should use what we have

It is a tidy story. Each plank is worth checking against the evidence.

Chapter 1: How much is actually left

The North Sea Transition Authority — the official UK regulator — publishes the figures each October. As of end-2024:

- Proven and probable reserves: 2.9 billion barrels of oil equivalent, down from 3.3 billion just a year earlier

- Total already produced since the 1960s: 47.7 billion barrels

- Peak oil production: 1999, when we pulled out roughly 6 million barrels a day

- Today: about 1 million barrels a day, falling to 660,000 by 2029 on the regulator’s own forecast

In four exploration wells drilled in 2024, the industry found less than 100 million barrels between them. Production outpaced new discoveries by more than four to one.

The Energy and Climate Intelligence Unit puts it plainly: about 93% of the cumulative North Sea total has already been extracted. Even on the oil-and-gas industry’s most optimistic “no constraints” scenario — which the industry itself accepts is unrealistic — you still end up with 86% already gone.

The relevant question here is not fossil fuels versus renewables. It is what to do with a depleted basin in structural decline, whatever anyone says about it.

Chapter 2: Why drilling more would not lower your gas bill

This is the part most often misunderstood, and it carries real consequences.

Oil and gas are globally traded commodities. A barrel of crude in Rotterdam, Cushing or the North Sea sells at the same world price, give or take quality and shipping. UK gas trades on the National Balancing Point, which moves in step with the European TTF hub. Our pipelines plug straight into Norway and the Continent.

If a UK operator pumps an extra million barrels out of the North Sea, it is under no obligation to sell that oil to British drivers at a discount. It sells it on the world market. In practice, about 80% of UK North Sea oil already gets exported, because British refineries are configured for sweeter, lower-sulphur grades. Only 7.7% of the oil refined in UK plants in 2024 came from our own waters, down from 50% in 1996.

The point does not rest on my word alone:

- The Climate Change Committee told government that increased UK extraction “would not materially affect global oil or gas prices”

- The UK Energy Research Centre said additional production would have “negligible impact on the UK cost of living”

- Oxford’s Smith School of Enterprise modelled it and found household bills could fall £16 to £82 a year (1–4.6%) under maximum extraction. By contrast, decoupling electricity prices from gas could cut bills by around £330 a year — three to four times more

The clearest test is Norway. It produces roughly twenty times more oil and gas per head than the UK does, and owns its reserves through a state-controlled company. Yet in winter 2022, Norwegian households paid some of the highest electricity prices in Europe, because Norwegian gas sells into the European market at European prices.

Domestic production does not insulate consumers when the commodity is freely traded.

Chapter 3: Who actually owns the oil

There is a quietly inconvenient fact here. Britain does not own the North Sea oil and gas. We own the seabed, but once a licence is granted, the hydrocarbons belong to whoever is operating the field — BP, Shell, Equinor (which is 67% owned by the Norwegian state), Harbour Energy, Ithaca Energy, TotalEnergies and a handful of others.

The UK takes its cut through tax. The current headline rate on North Sea profits is 78% — corporation tax (30%) plus a supplementary charge (10%) plus the Energy Profits Levy (38%, running until 2030). That is a high rate, but the basin is also generous with reliefs for decommissioning costs.

Tax receipts in context:

- Peak: £12.4 billion in 2008/09 (worth around £18 billion in today’s money)

- 2022/23: £9 billion (post-Ukraine spike)

- 2024/25: £4.5 billion

- Forecast 2025/26: £2.7 billion

Compare that with Norway’s sovereign wealth fund — the result of taxing and state-owning its oil — which now stands at over $1.5 trillion. Estimates of what Britain could have built had it copied Norway run from $400 billion to £850 billion, or about £13,000 for every person in the country. That opportunity passed in the 1980s, but it is worth remembering when politicians describe North Sea oil as “Britain’s birthright”. Largely, it is not.

Chapter 4: What about the new fields — Rosebank, Jackdaw, Cambo?

These are the headline projects the “drill more” lobby points to.

Rosebank, west of Shetland: about 300 million barrels recoverable, mostly oil. First production scheduled for late 2026. Plateau output around 70,000 barrels a day for two or three years before decline. For scale, that is roughly 1% of UK gas demand (the field is 90% oil), and the oil is the wrong grade for UK refineries, so most of it will be exported.

Cost: around $3.8 billion in capital investment for Phase 1 alone. It is the deepest field ever developed on the UK Continental Shelf, sitting in over a kilometre of water in some of the harshest conditions in the Atlantic.

Jackdaw (Shell): a smaller gas project, also in legal limbo.

Cambo (Ithaca Energy): final investment decision now slated for 2026/27, first oil “late 2020s or early 2030s”. Shell pulled out in 2021.

In January 2025, the Court of Session in Edinburgh ruled the Rosebank and Jackdaw consents unlawful because the environmental impact assessments had not accounted for combustion emissions. This followed a Supreme Court ruling, R (Finch) v Surrey County Council, in which Lord Leggatt set out the point:

“It is known with certainty that, if the project goes ahead, all the oil extracted from the ground will inevitably be burnt thereby releasing greenhouse gases into the earth’s atmosphere in a quantity which can readily be estimated.”

The legal point can be argued either way, but the practical result is that any new field now has to count what happens when its product is burned. That changes the arithmetic.

Chapter 5: The cost of getting it out

The North Sea is one of the more expensive basins in the world to operate.

- UK Continental Shelf operating cost: £19.49 per barrel in 2024 (NSTA)

- Saudi Arabia: roughly $7-9 per barrel

- OPEC median: about $5.40 per barrel

- US shale: $46-54 breakeven

The reasons are smaller fields, deeper water, ageing infrastructure, and more people on board per barrel produced. Costs rise as output falls, because fixed costs are spread across fewer barrels.

Then there is decommissioning — the unavoidable bill for plugging wells, removing platforms and clearing pipelines when fields close. The NSTA estimates this at £44 billion in total, with around £27 billion of it falling between 2023 and 2032. Wood Mackenzie noted that “over £17 billion will be spent on UK decommissioning by 2029 — twice that of any other country”.

A portion of that bill lands on the taxpayer, because operators can offset decommissioning costs against past tax paid. The NSTA itself has flagged about £10.8 billion in lost taxes from accelerating decommissioning. The “free oil” is not free.

Chapter 6: Renewables and the intermittency problem

This is the strongest plank in the “drill more” argument, and it deserves a fair hearing.

Wind does not blow on demand. Solar does not generate at night. In a still January high-pressure week, you can look at a UK weather chart and feel genuine unease about where the electricity is going to come from.

Here is what the data says about how the UK is actually managing it:

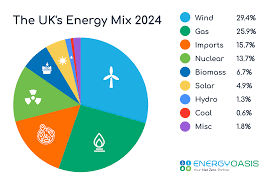

- 2024 electricity mix: renewables 50.4%, nuclear 14.3%, gas 30%, imports the rest. The first full calendar year with renewables above half

- Offshore wind capacity factor: 40.5% in England in 2024, forecast to rise to about 57% by 2030 with bigger turbines

- Battery storage on the grid: from 4.5 GW at end-2024 to 6.9 GW by end-2025, with a target of 23-27 GW by 2030

- Interconnectors to France, Norway, Belgium, Netherlands, Denmark, Ireland: about 9-10 GW of two-way capacity

- Pumped hydro: 2.8 GW (Dinorwig in Wales does 0-1.7 GW in 16 seconds)

- The last coal plant, Ratcliffe-on-Soar, closed on 30 September 2024

Gas is still essential as a backup, and will be for years; nobody serious disputes that. The question is whether gas should be the foundation of the system or the safety net for it.

On cost: new offshore wind in the most recent auction (AR7, January 2026) cleared at around £91 per MWh in 2024 prices. New gas-fired power costs around £147 per MWh on current build prices. New nuclear (Hinkley Point C) is contracted at £92.50 per MWh in 2012 money — about £128 per MWh today, for 35 years, with construction now running £46 billion against an initial £18 billion estimate.

On those figures, renewables are now the cheapest new-build power in Britain — not cheap once subsidies kick in, but cheapest outright. That does not resolve intermittency on its own. It does mean that, whenever someone says “renewables are too expensive”, the auction data points the other way.

Chapter 7: Could clean power genuinely do it?

The answer is yes for electricity, and harder for total energy.

Electricity is currently about 20% of total UK final energy use. The other 80% — heating, transport, industrial heat — is mostly fossil-fuelled. The transition the Climate Change Committee maps out does not merely decarbonise electricity. It electrifies everything else: heat pumps replacing gas boilers, EVs replacing petrol cars, hydrogen and electric arc furnaces replacing industrial gas burners.

That requires electricity demand to roughly double or treble by 2050, and offshore wind to grow from today’s 16 GW to over 100 GW. It is a large build-out. On the CCC’s numbers it is also achievable, at a net cost of less than 1% of GDP cumulatively over thirty years.

Where the strain genuinely shows:

- Grid connections: there are projects waiting years to plug in

- Planning: onshore wind in particular has been bogged down for a decade, only just unblocked

- Supply chain: offshore wind supply chains are stretched globally, pushing recent prices up

- Skilled labour: electricians, grid engineers and offshore technicians are all in short supply

These are real bottlenecks. They are not reasons the transition cannot happen. They are reasons it requires genuine industrial strategy rather than slogans.

Chapter 8: Jobs, Aberdeen, and the human cost

This is where the “drill more” argument has its most legitimate weight, and it deserves to be taken seriously rather than waved away.

The oil and gas industry trade body says it supports 154,000 jobs across the wider offshore energy sector, with about 84,000 in Aberdeen and Aberdeenshire alone. Other counts (the ONS) put direct employment closer to 28,000. The real figure sits somewhere in the middle once you count contractors, supply chain and induced employment.

Robert Gordon University projects the UK oil and gas workforce will fall from 115,000 in 2024 to between 57,000 and 71,000 by the early 2030s — a roughly 50% decline regardless of what any politician says. That decline is structural, driven by the basin being mostly empty, not by net zero policy.

The right policy question is not whether we save these jobs, since they are going whatever happens. It is whether we use the next decade to make sure these workers move into the offshore wind, hydrogen and CCS jobs that are physically growing in the same waters, using overlapping skills.

The current government’s North Sea Future Plan (November 2025) puts £20 million into retraining and an Energy Skills Passport. Whether that is enough is a fair argument. Whether the transition is happening at all is not.

Chapter 9: Where the “energy independence” argument breaks

It is worth being specific about what energy independence would actually mean.

To be genuinely independent on oil, the UK would need to:

- Produce all its own oil (we don’t, and can’t — the basin is too depleted)

- Refine it domestically (we partly can’t — wrong grades for our refineries)

- Sell it domestically at non-world prices (we can’t — companies sell where prices are highest, which is the global market)

To be genuinely independent on gas, we would need to:

- Produce all our own gas (we currently produce about half)

- Be physically disconnected from the European market (we are plumbed into it via three pipelines)

- Have enough storage to ride out shocks (we have about 12 days; Germany has 89, France 103, Netherlands 123)

The realistic version of energy independence is not about producing more oil and gas. It is about needing less oil and gas — through electrified heating, transport and industry, with enough domestic clean generation and storage to absorb whatever the world market does.

That is not a green talking point but a straightforward strategic logic. Every kilowatt-hour you do not need to buy on a volatile world market is a kilowatt-hour of energy security.

Chapter 10: The verdict

The political argument for ramping up the North Sea has emotional appeal and genuine force on the jobs question. The engineering, economic and market evidence, though, cuts hard against it on its central claims.

On reserves: the basin is roughly 93% drained. What is left is expensive, technically complex, and will not change the strategic picture.

On prices: drilling more here does not lower prices here. Oil and gas are global commodities. Norway demonstrates the point, as does the wider data.

On security: even doubling production would not deliver independence, because we do not own the oil, cannot refine most of it, and cannot decouple from European gas markets. Reducing demand is a faster route to security than chasing depleted reserves.

On renewables: they are now the cheapest new power. Intermittency is a real engineering challenge with real engineering answers — interconnectors, storage, pumped hydro, demand response, and gas as backup. The build-out is happening, slower than ideal but faster than critics admit.

On jobs: the workforce transition is happening with or without policy, because the basin is running out. The question is whether we manage it well or badly.

None of this makes net zero free, easy or politically painless. Nor does it mean every oil and gas decision is automatically wrong. Some tieback projects to existing infrastructure produce gas at lower emissions intensity than imported LNG and are defensible on transition grounds.

But the larger argument — that we should abandon the clean energy push and bet the economy on a depleted basin — does not survive contact with the numbers.

The North Sea has served Britain well for sixty years. It is tired. Our energy future will come from somewhere else, and the sooner we accept that, the better prepared we will be for whatever comes next.

Sources for this piece include the North Sea Transition Authority, Climate Change Committee, Office for Budget Responsibility, HMRC, DESNZ, Carbon Brief, the Oxford Smith School, Wood Mackenzie, Offshore Energies UK, the Energy and Climate Intelligence Unit, the Supreme Court (Finch v Surrey CC), and the Court of Session. A full evidence dossier is available as a companion document.

Comments

No login needed. Comments are moderated before publishing.